The seasons again have a stronger impact on the market. The housing market is moving steadily, but the pace of sales in growth centres is accelerating at a somewhat slower pace than in other areas. The outlook for interest rates and employment is slowing down. Many homebuyers even expect interest rates to fall when renting. “Since the clearest upward turn will come, it is difficult to predict accurately,” comments Jussi Mannerberg, CEO of Finnish Real Estate Agents SKVL. “Late autumn is often a bit quieter anyway, and now it looks like the buyer’s market will be over next year,” he continues. “Now more than ever, it’s worth buying your own apartment when the supply is better and the price level has bottomed out,” Mannerberg adds. “In late autumn, we may still see a slight decrease in demand in some areas, and consequently a 2–3% decrease in actual prices, but not in the most demanded housing types,” he sums up.

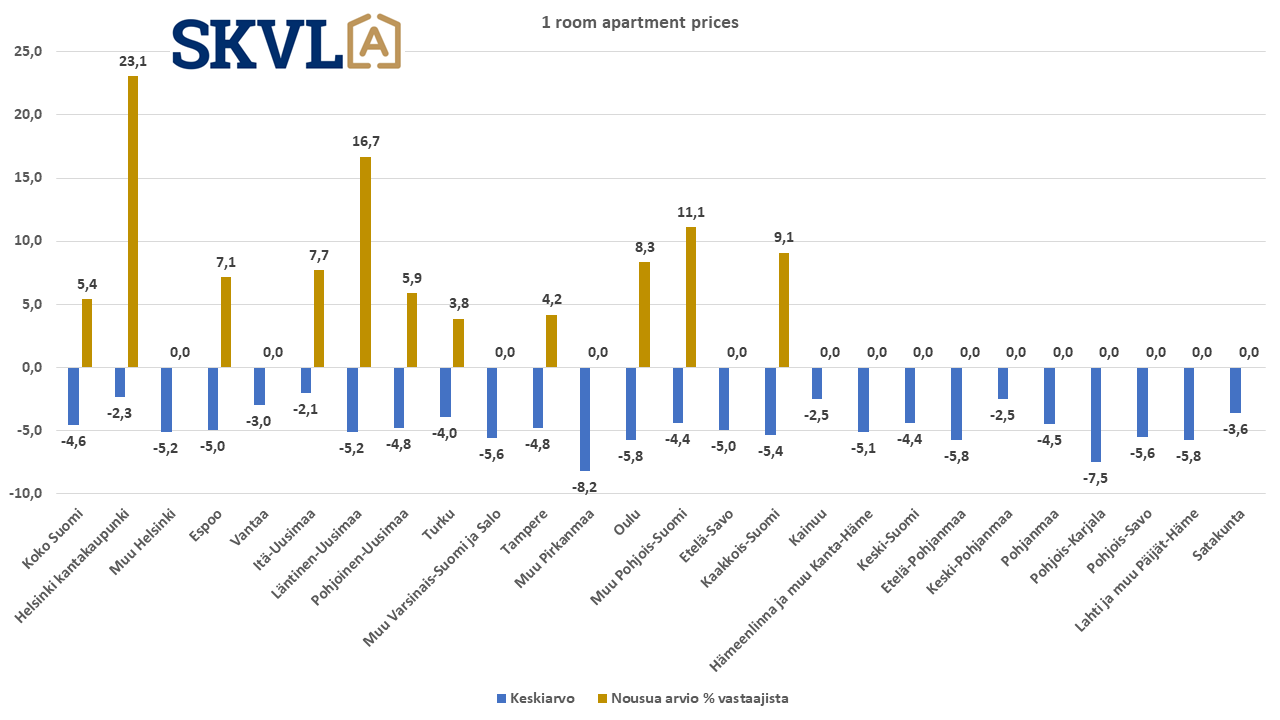

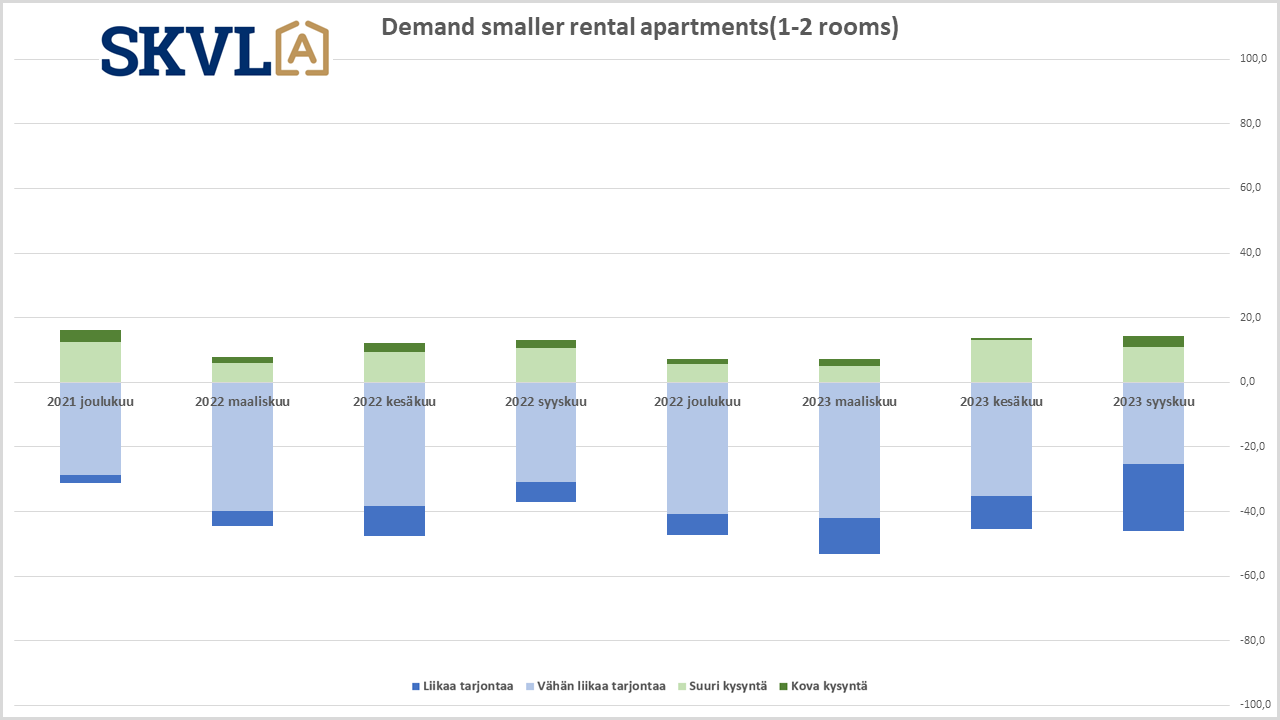

The latest increase in the key interest rate slowed down housing sales in September – downward pressure continues on the prices of small dwellings due to oversupply

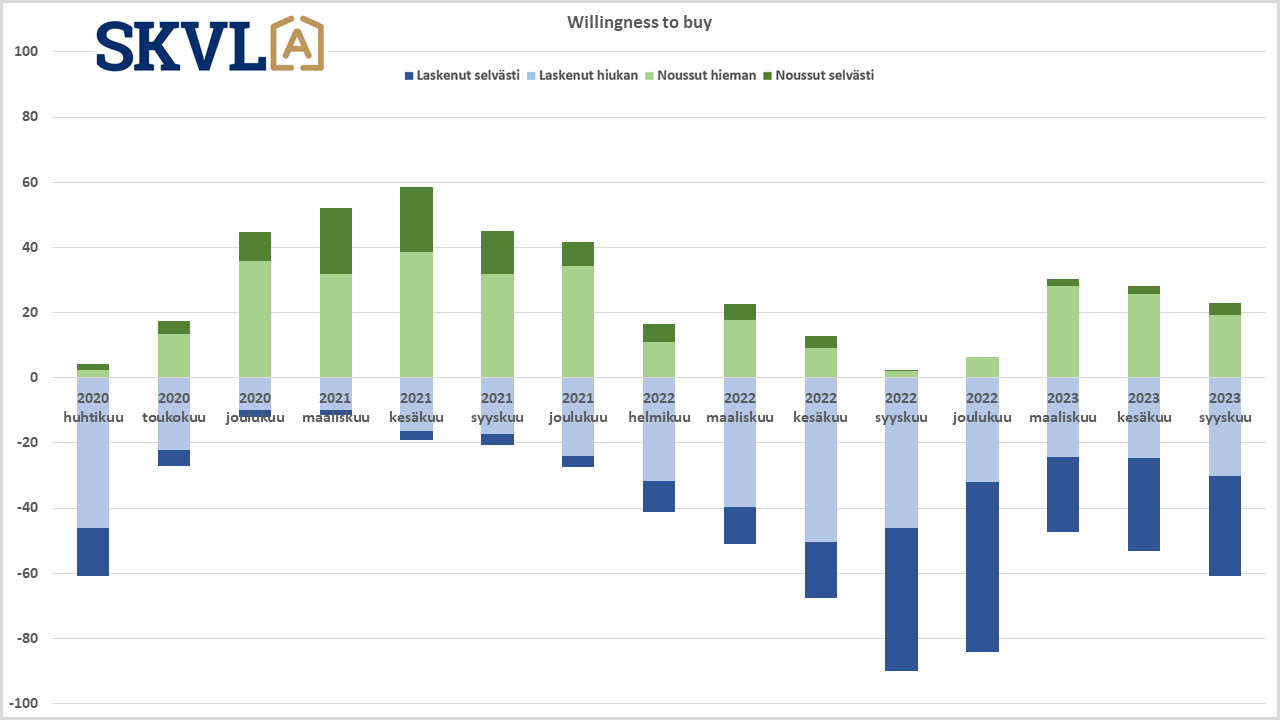

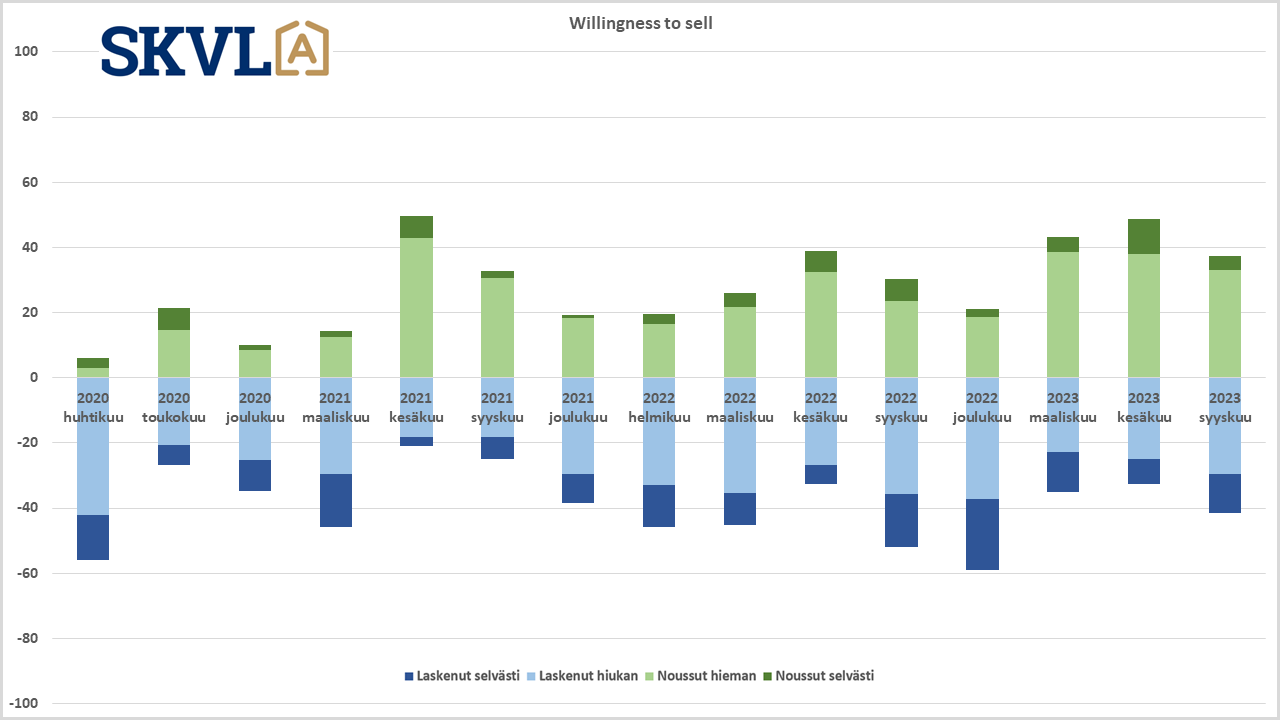

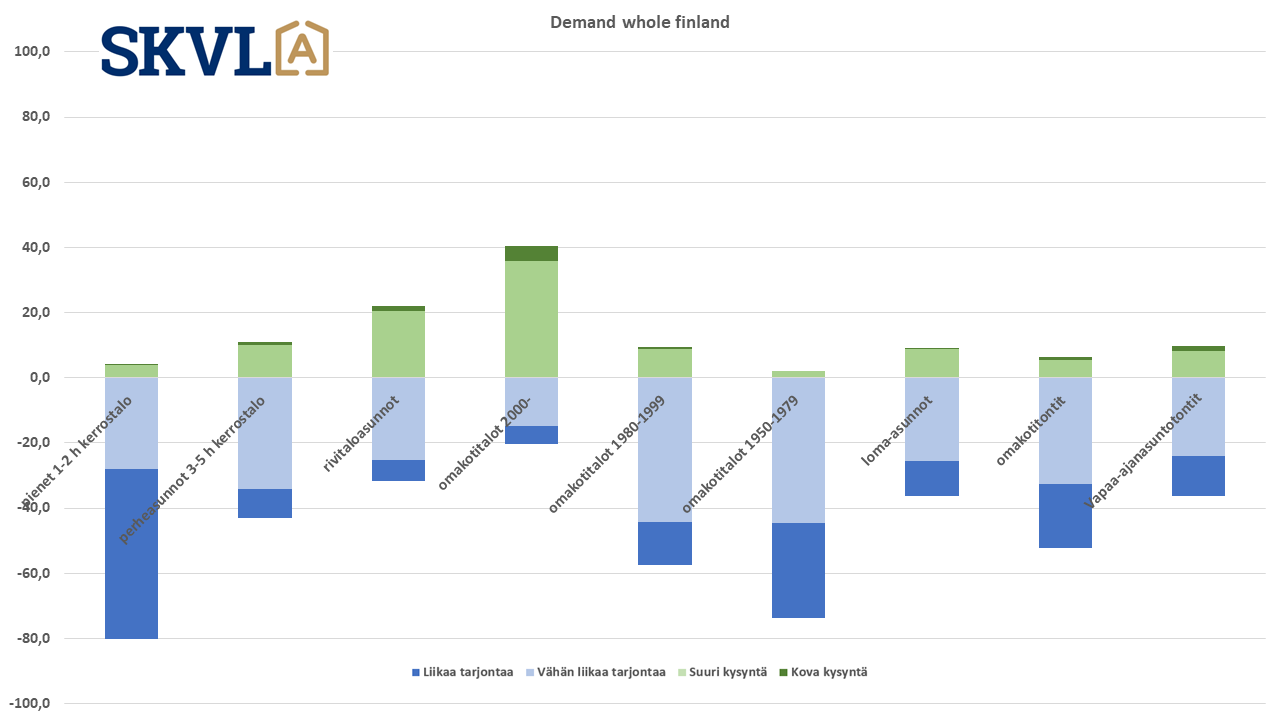

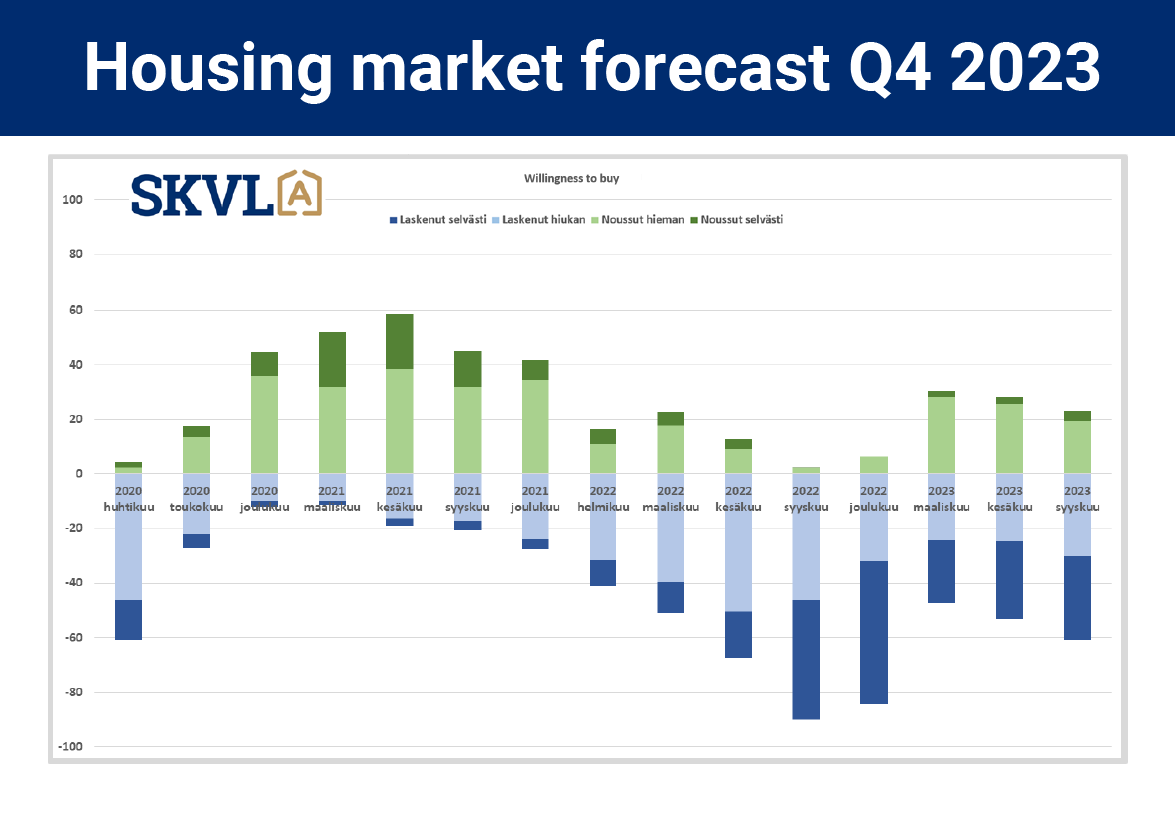

Buying pressure is increasing, but many are waiting for interest rates to turn downwards. “Market news has created the impression for some buyers that you can offer anything about apartments. However, this does not lead to any deals, but rather stops negotiations with the buyer in question,” comments Mannerberg. The relationship between supply and demand, which primarily guides house prices, is currently fairly well balanced. With the exception of the smallest dwellings in blocks of flats and older detached houses, where demand is clearly lower. The “willingness to buy a home” indicator regularly measured by SKVL is now clearly higher than a year ago, when the market slowed down. The “seller motivation” indicator is also clearly higher, although it has decreased slightly since the summer.

Transfer tax and deduction for interest on housing loans

“It is understandable that Finland’s indebted economy is in a challenging situation and the Government’s means are limited,” comments Mannerberg. “It is possible that some home buyers are even waiting for the transfer tax to be abolished,” he continues. “It is very important that the government sends a stronger message about this as soon as possible. Either a decision is made or not, the current situation could potentially slow down trade,” he continues. Reinstating the mortgage interest deduction would be an even better remedy for the period when interest rates are this high. An increase in trade would certainly create more employment, for example, in the construction sector and thus increase compensatory tax revenue. “The decline in inflation in Finland and the EU area has now been so rapid that it is high time for the ECB to cut its key interest rates as soon as possible,” Mannerberg adds.

Improved access to credit – processing times still long

SKVL has received reports that housing loan processing times are still quite long. There has also been a message that loans can currently be negotiated better, both for existing debtors and for new borrowers. Banks are now more prepared to grant housing loans, at least in growth centres. Now it is worth actively bidding for loans. The big challenges for smaller towns are still financing older houses and apartments that are being renovated. State assistance is urgently needed for the availability of renovation loans and their guarantees.

The Finnish housing market has suffered more than many other EU countries

In many countries in the EU area, house prices have hardly fallen and demand has remained better than in Finland. House prices in Finland are currently lower than average on the European level. An upward correction is expected in Finland as interest rates begin to decline and demand recovers. Foreign buyers’ interest in Finland is also on the rise, both in terms of apartments and holiday homes. “We are currently in a peculiar period of stagnation, which is starting to unravel as interest rates fall and both buyers and sellers have understood the market situation,” Mannerberg adds.

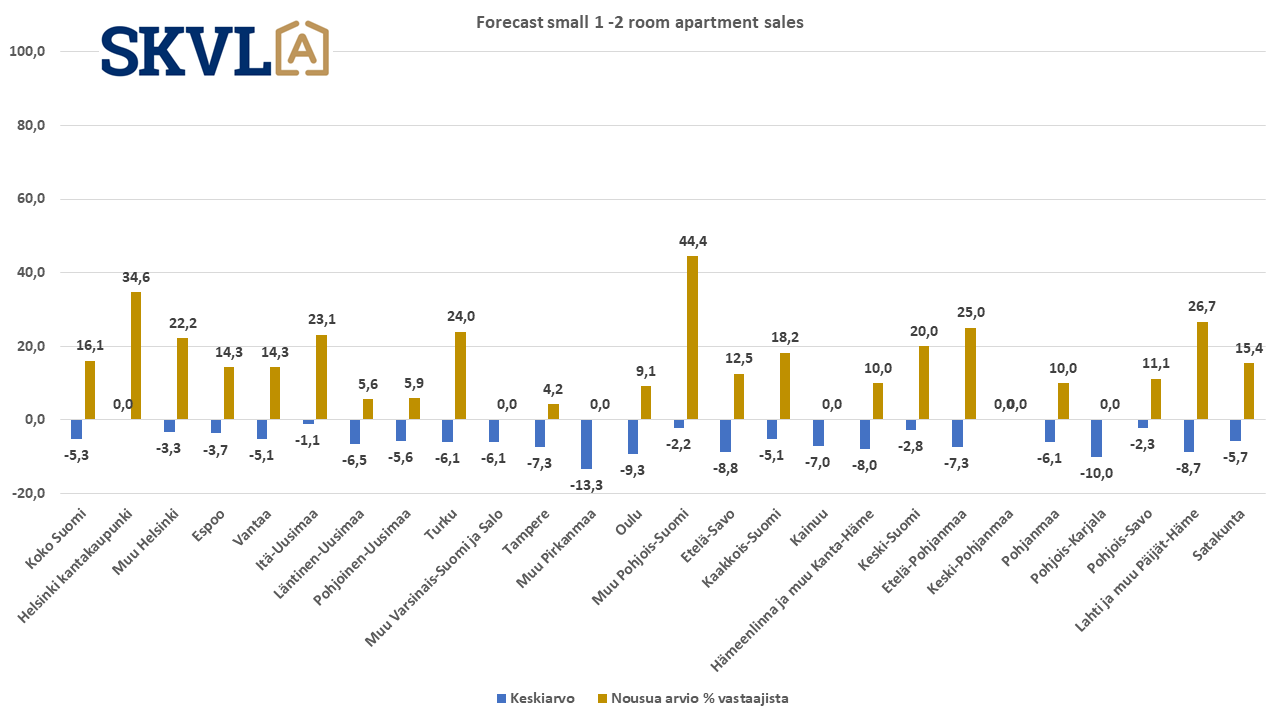

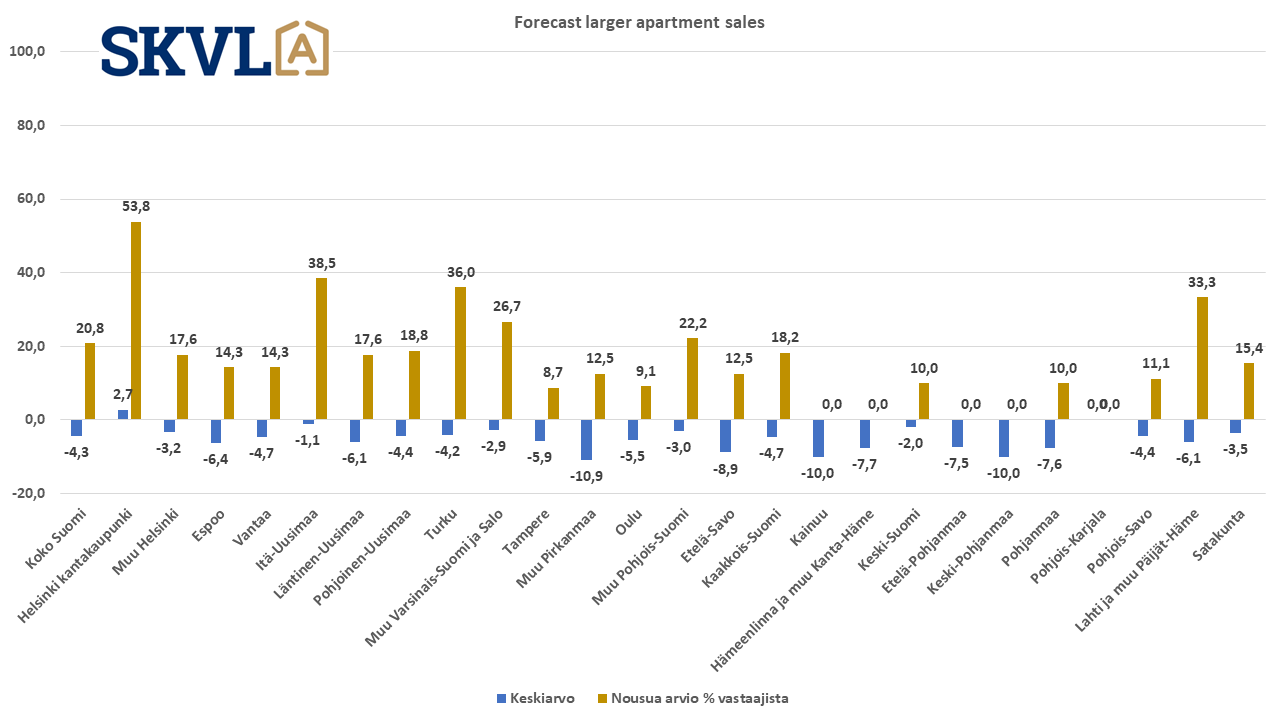

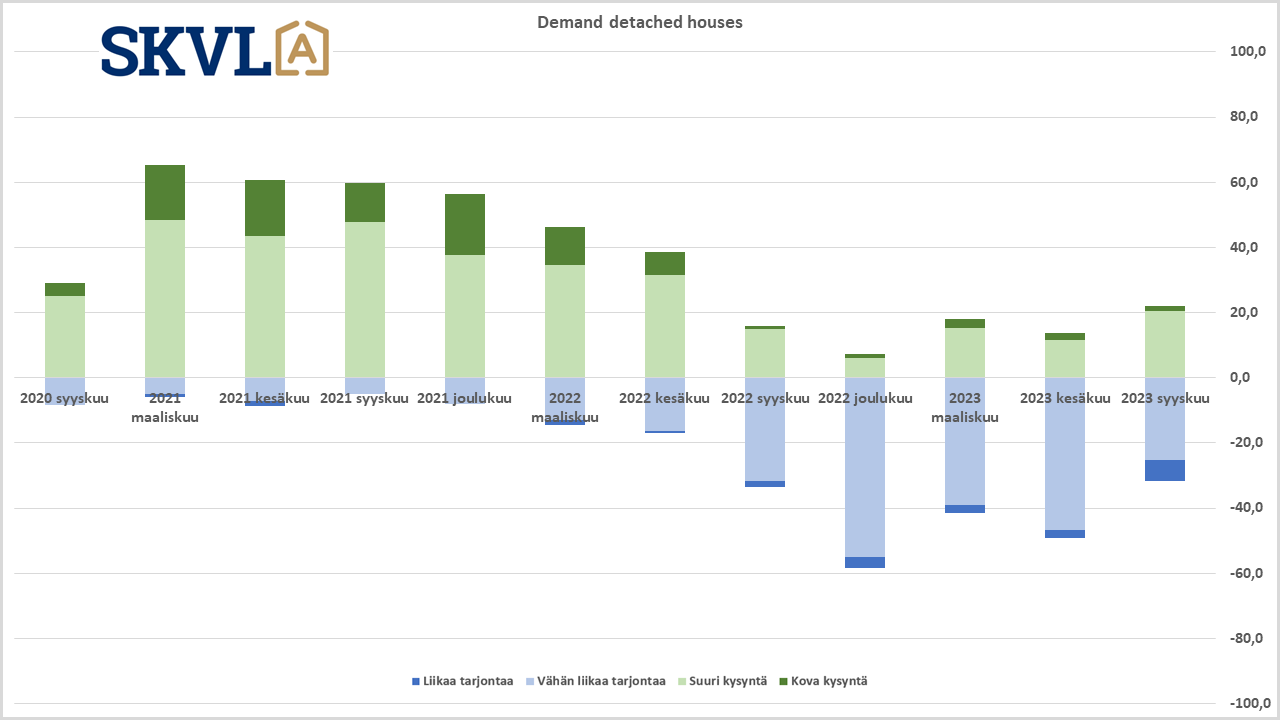

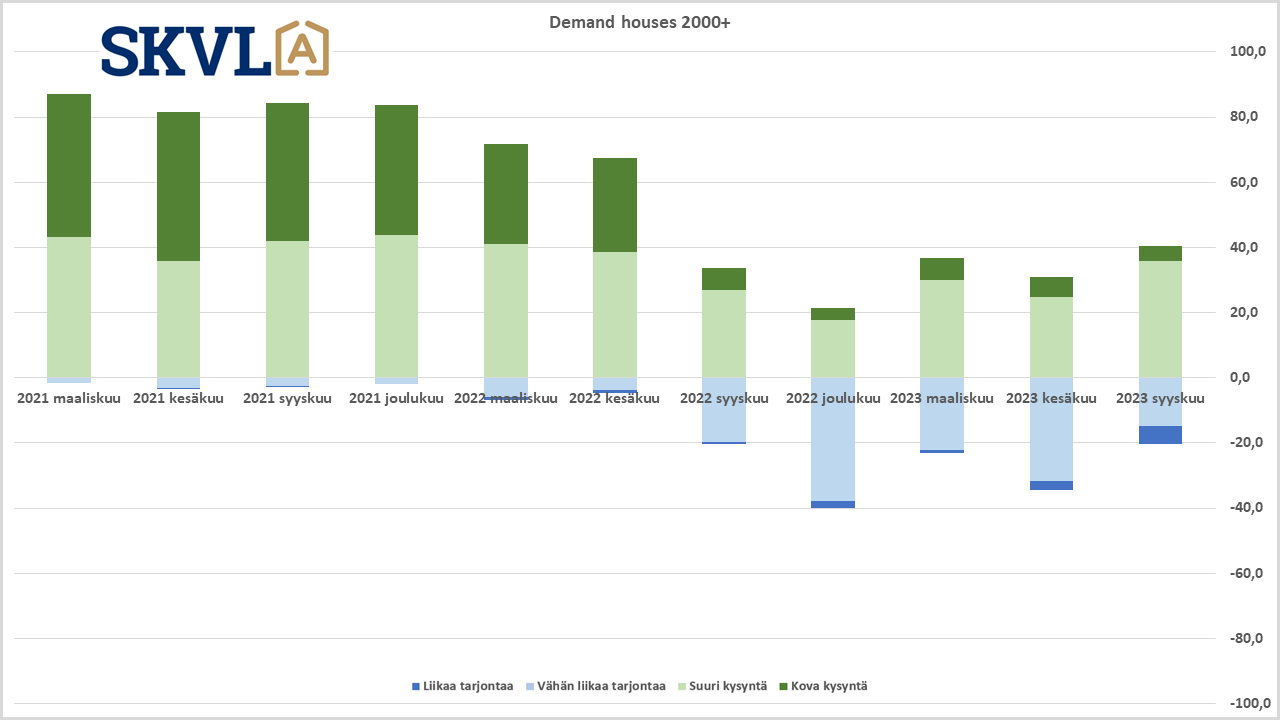

Sales of new properties are expected to remain subdued and downward pressure on prices

The appeal of new properties in the housing market will continue to be small this autumn. In normal market conditions, the higher price level of new dwellings affects the prices and desirability of the areas. In the current market, the wait will still take a while, but the recent increase in construction costs will lead to a higher price level for new start-ups. As early as next year, we will see a new price level in new dwellings, which will also have an upward impact on the prices of old dwellings.

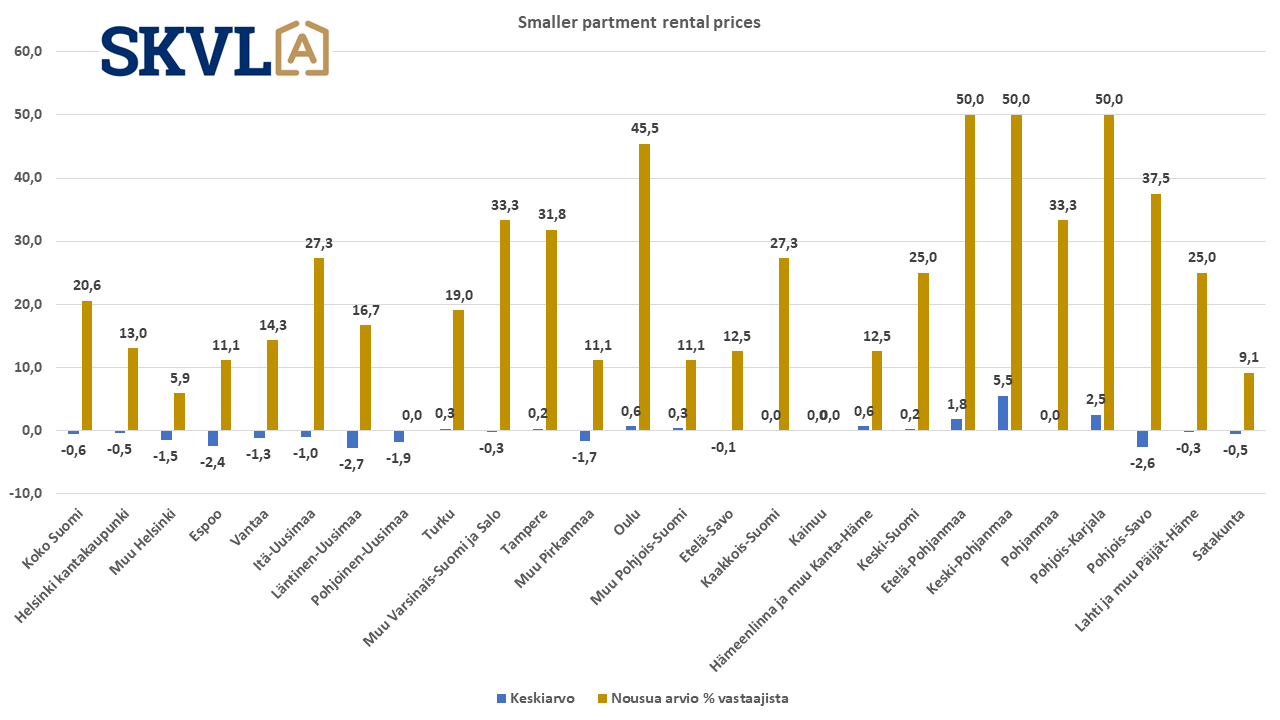

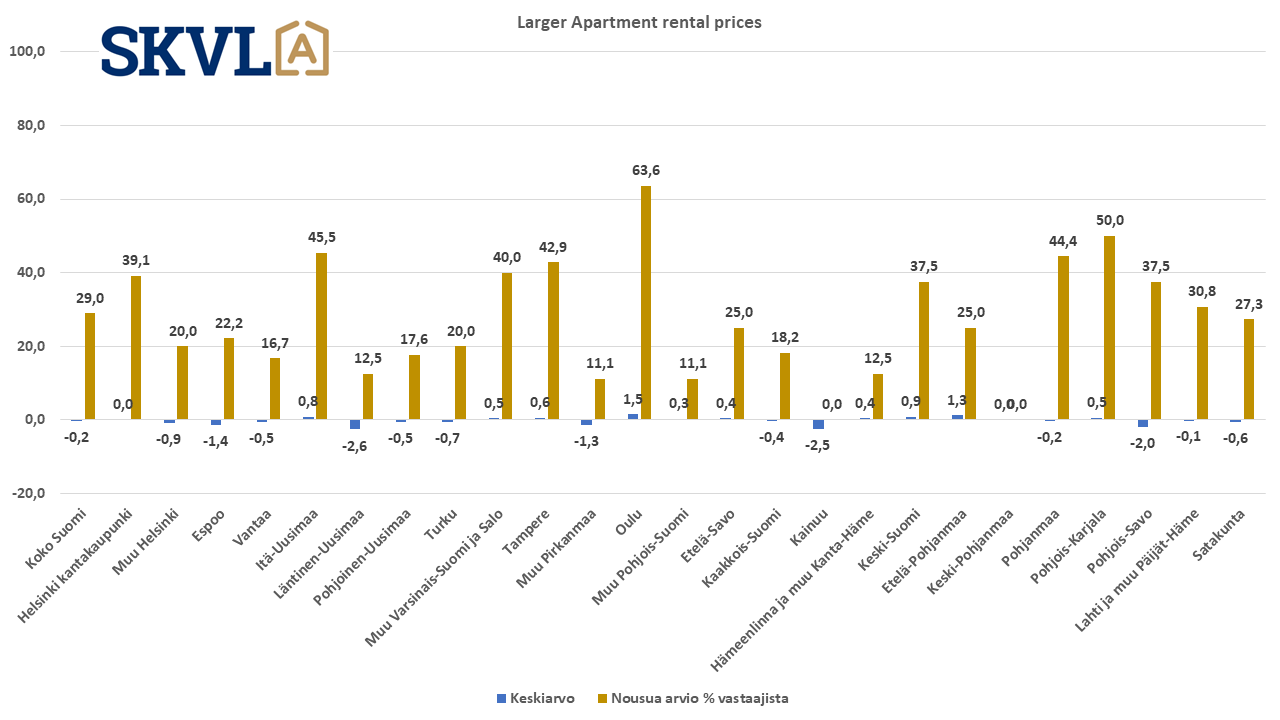

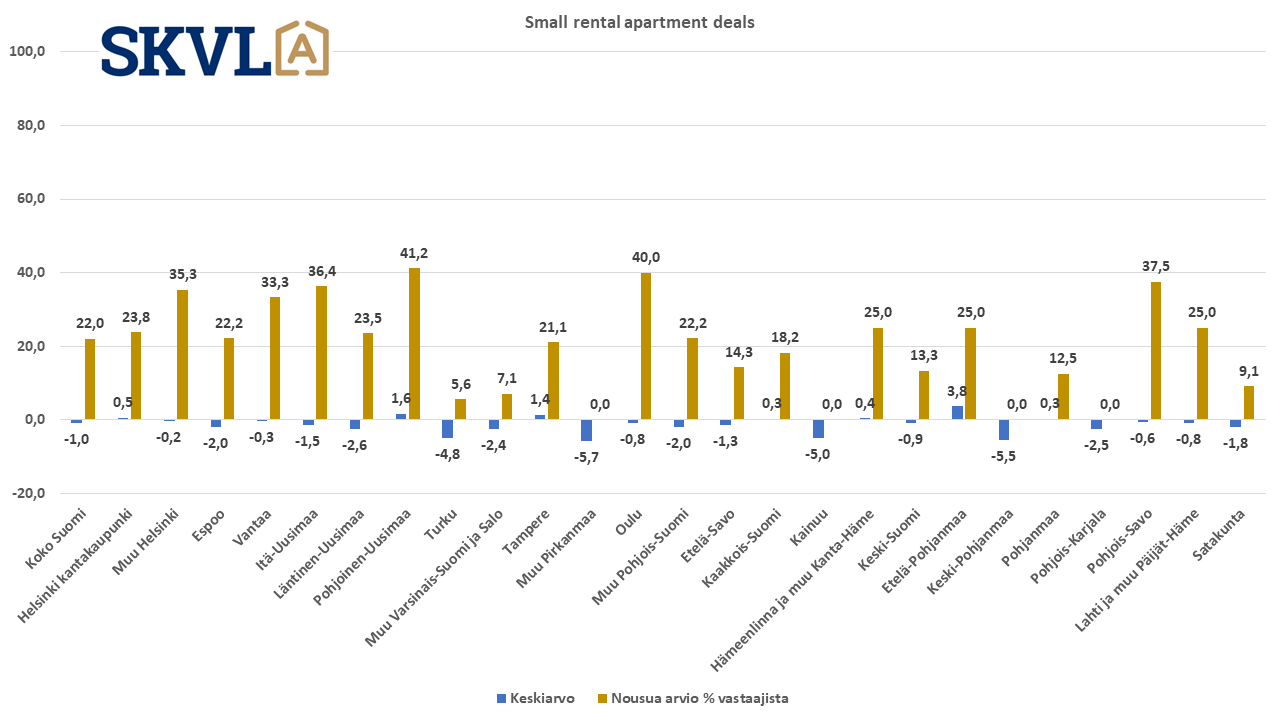

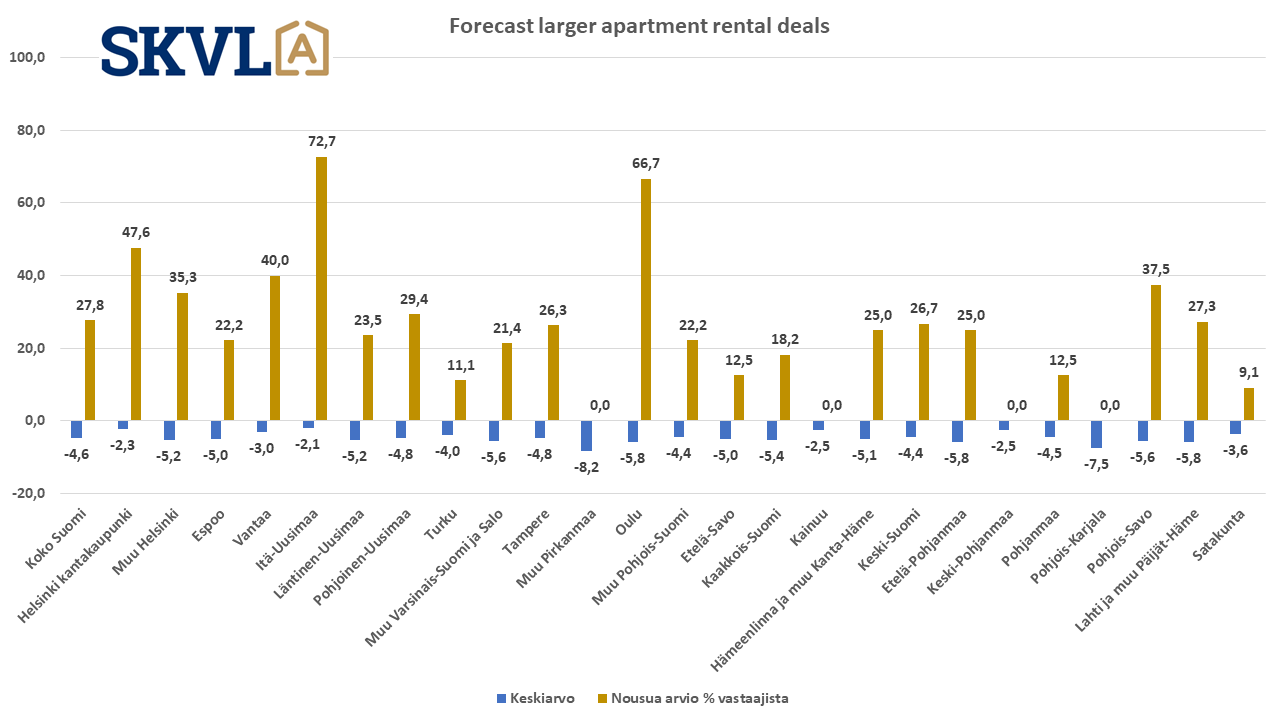

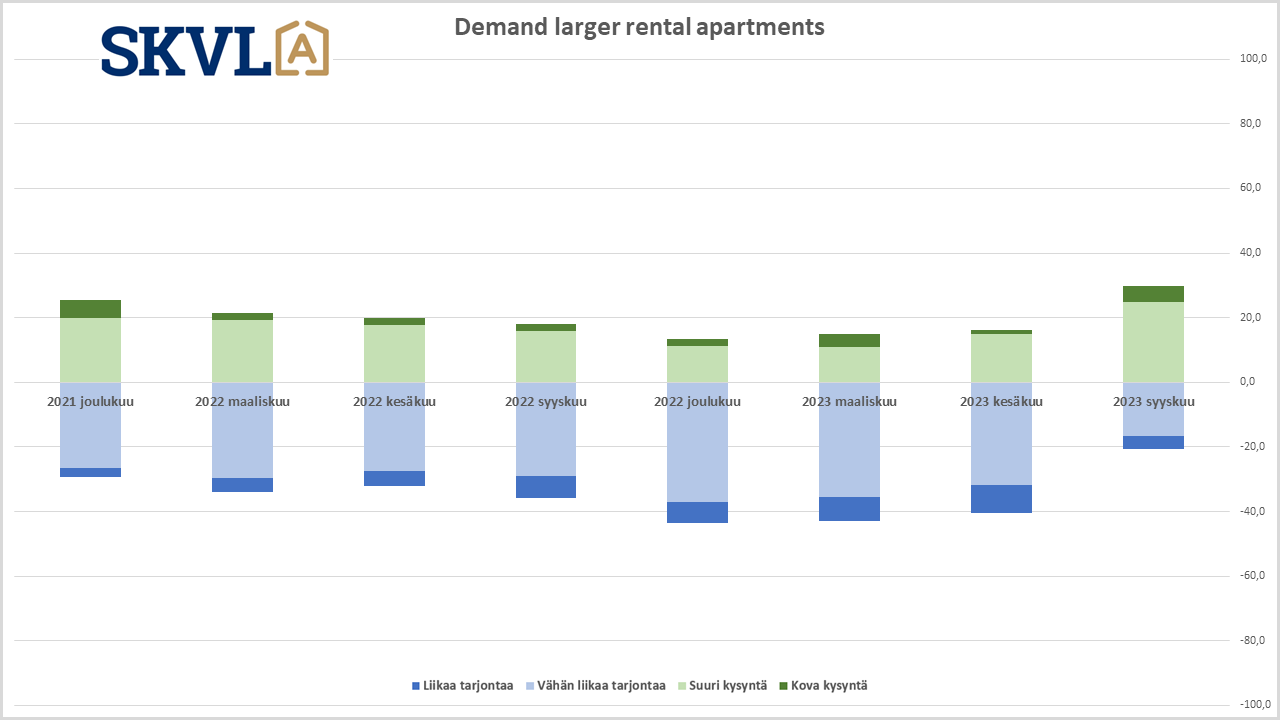

In rental apartments, a large supply calms the rise in rents

The supply of rental housing is historically high. Demand has also risen somewhat, but not so much that there is competition for housing. However, there are areas in Finland, such as holiday resorts in Northern Finland, where there is a shortage of smaller rental apartments. There is a steady demand for larger, good rental apartments everywhere and their supply is not sufficient. The rise in interest rates and maintenance charges will be visible next year as upward pressure on rents, but no significant changes are forecast for this autumn.

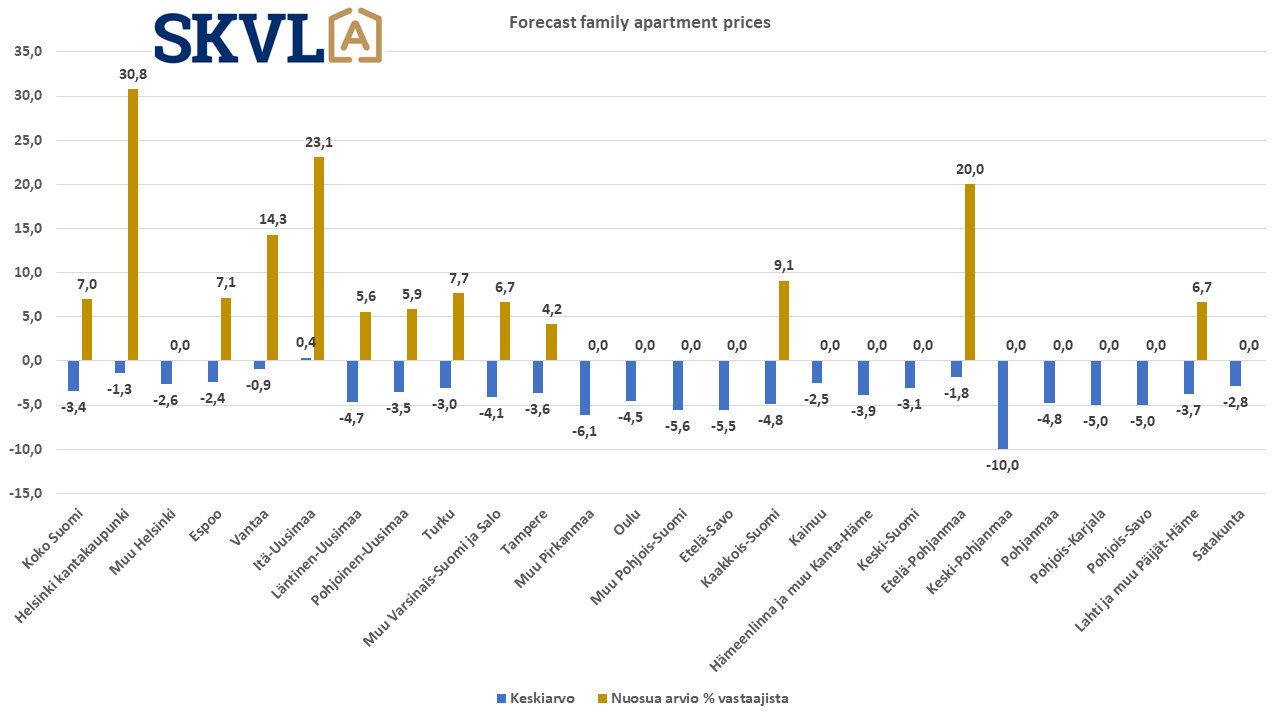

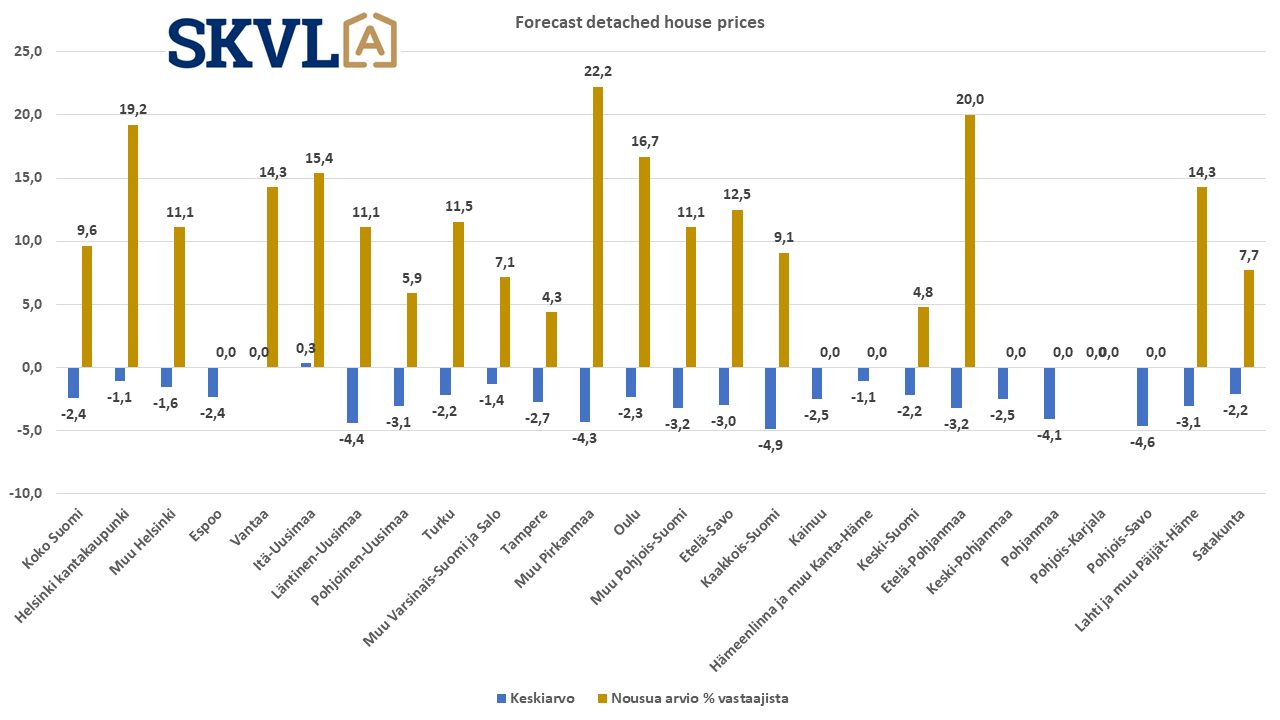

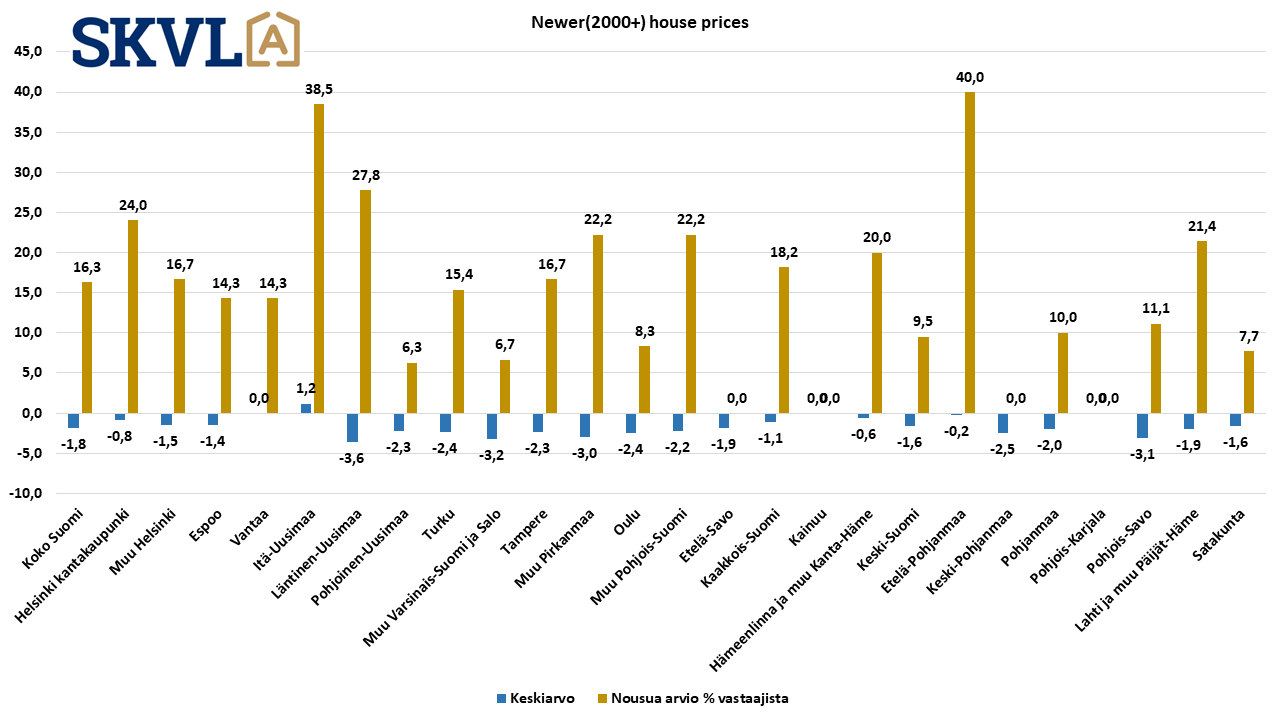

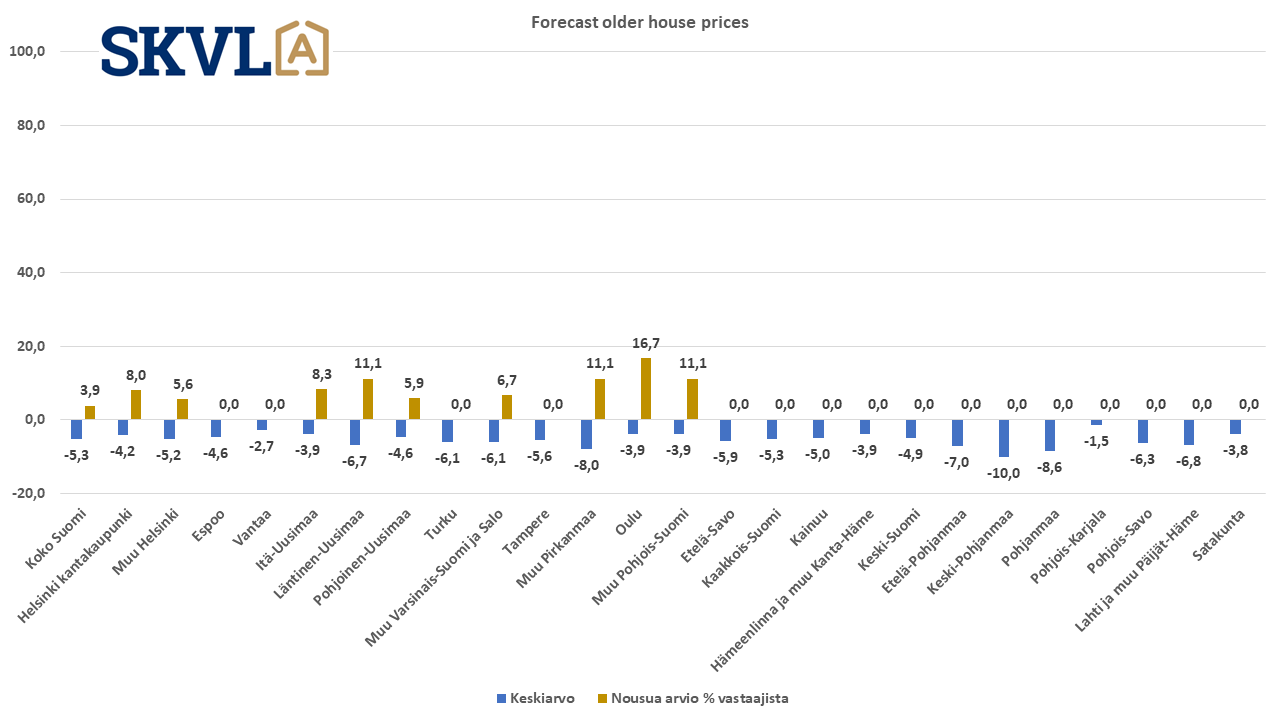

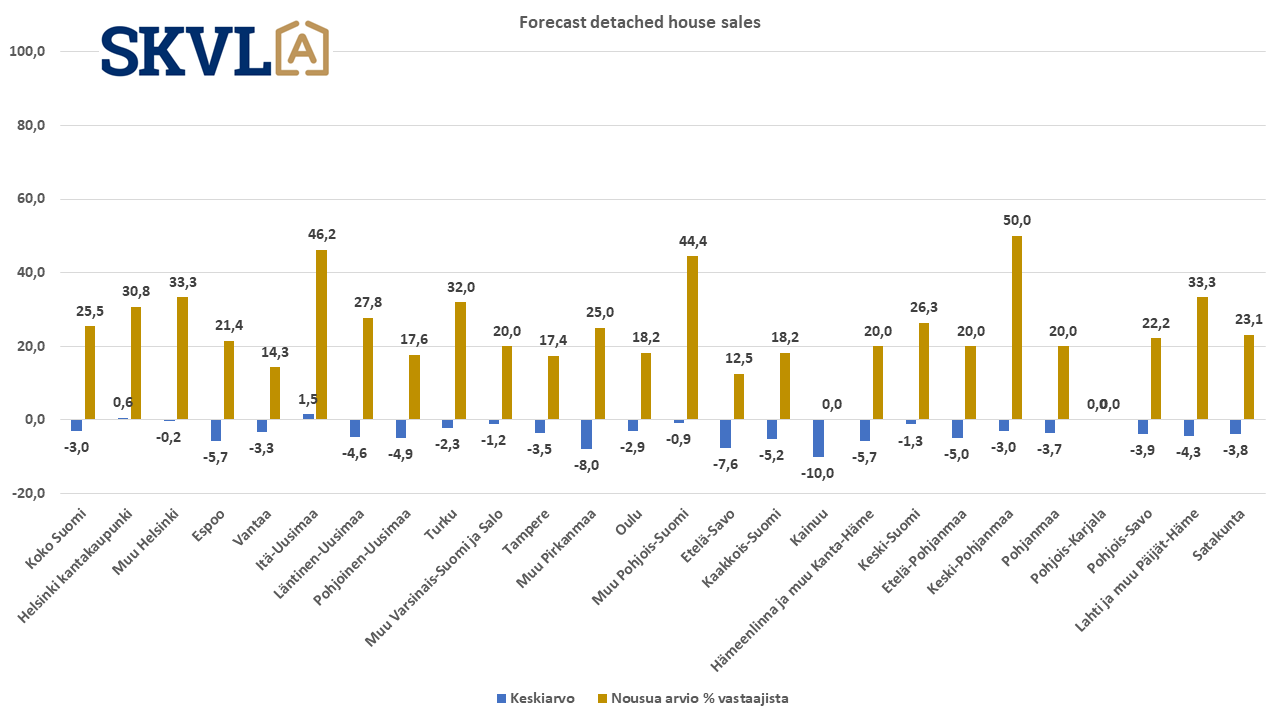

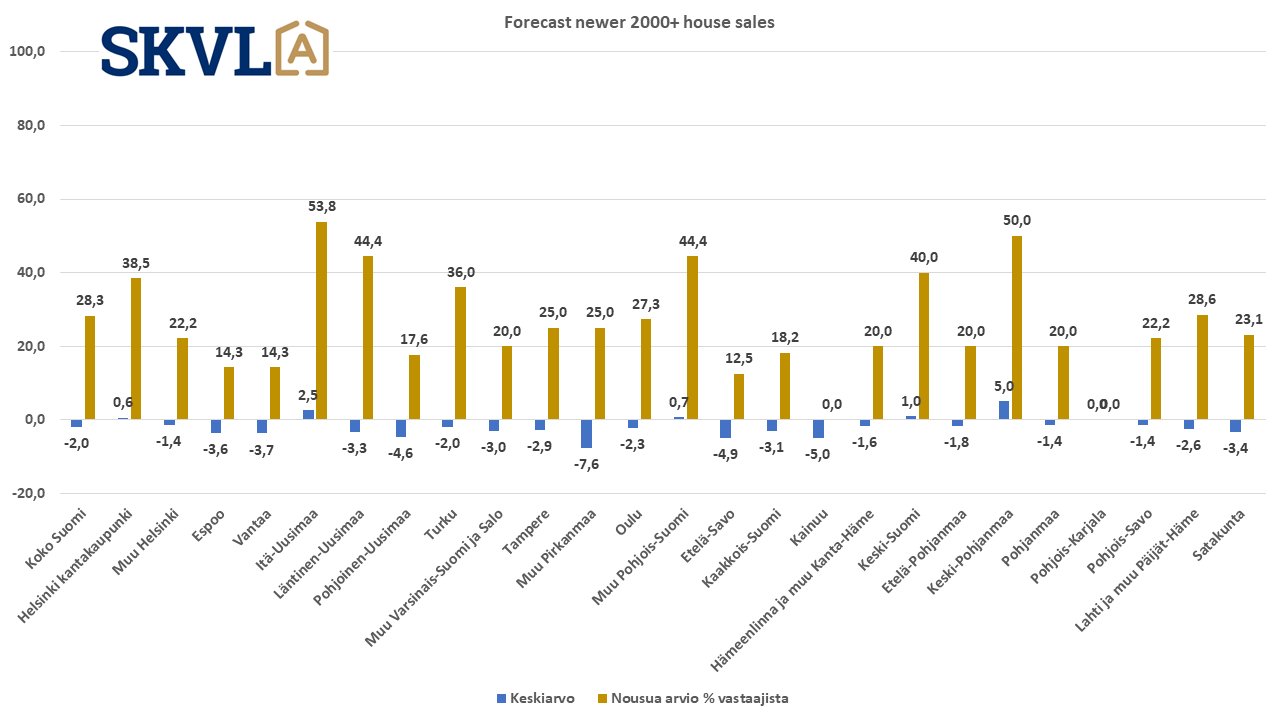

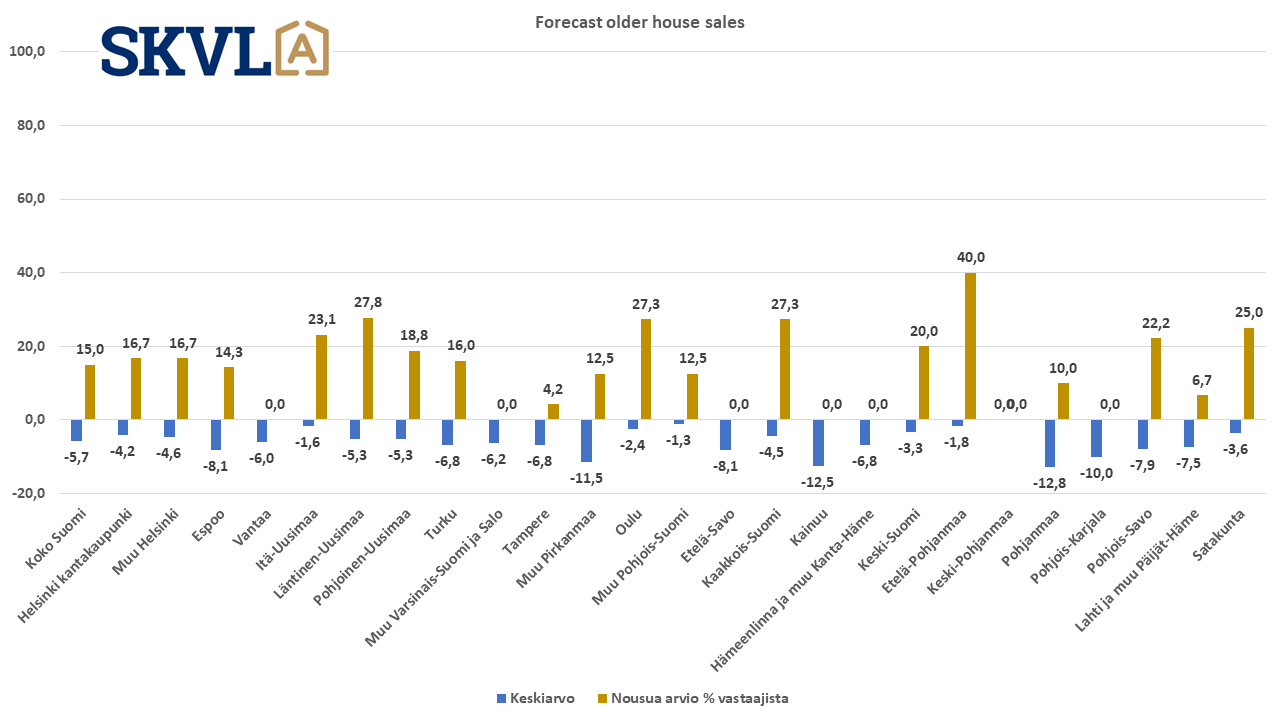

Regional comments SKVL housing market forecast 2023 end of the year

Helsinki, inner city

The demand for apartments of different sizes in Helsinki and the rest of the city centre has increased slightly. Valuable apartments are also being looked at and their sale has started. Furthermore, the sale of buyers’ own apartments is often a condition of the offers. Sales of small apartments have also taken off in the inner city. To some extent, sellers still have fairly high expectations of sales prices, which, however, have clearly decreased compared to two years ago. Currently, there is a lot of supply and there are good opportunities for buyers to find a suitable type of housing. Lauttasaari is somewhat quieter and has a lot to offer.

Rest of Helsinki

Demand for small apartments remains low, but demand for family homes is improving. Sales of apartments in renovated properties and housing companies with renovation debts are quieter. The demand for apartments in good condition has returned.

Espoo

The market situation in Espoo is somewhat quieter than elsewhere in the Helsinki metropolitan area. However, deals are being made and newer houses with geothermal heat are selling better. There are still challenges in selling renovated properties. All in all, the situation in Espoo is waiting.

Vantaa

In Vantaa, sales of small apartments in particular are quiet. Demand is good for terraced houses and detached houses in good condition. Demand for housing companies undergoing renovation and renovation is still lower.

Eastern Uusimaa

In Eastern Uusimaa, there has been more demand in Porvoo, Loviisa and Sipoo in the summer, and sales times have shortened and sales volumes have increased, prices have come down. In Porvoo, single-family houses in good condition sell best, buyers mainly come from the Helsinki metropolitan area.

Western Uusimaa

In Hanko, the peak season begins to slow down with autumn, but buyers are still on the move. The price level has fallen somewhat – with realistic prices, apartments will move in winter. In Hanko, apartments are often bought as second homes, so selling one’s own apartment is not an obstacle. In Kirkkonummi, with houses with yards in the 2000s and a good form of heating, demand is strong. Trade in the Vihti area is good nicely, there are a lot of contacts. There is a high demand for single-family houses in Karkkila. Buyers in the Helsinki metropolitan area are looking for apartments further away from the city centre, in search of lower prices and quality of housing.

Northern and Central Uusimaa

In Nurmijärvi, trade is nice. Family apartments in good condition are in particular in demand. In Mäntsälä, trade is still quiet. In Hyvinkää, there are differences of opinion on sales prices. Sales of houses to be renovated in Kerava and Järvenpää are quiet, and there is also little demand for newer apartment buildings. Prices often do not meet buyers’ expectations.

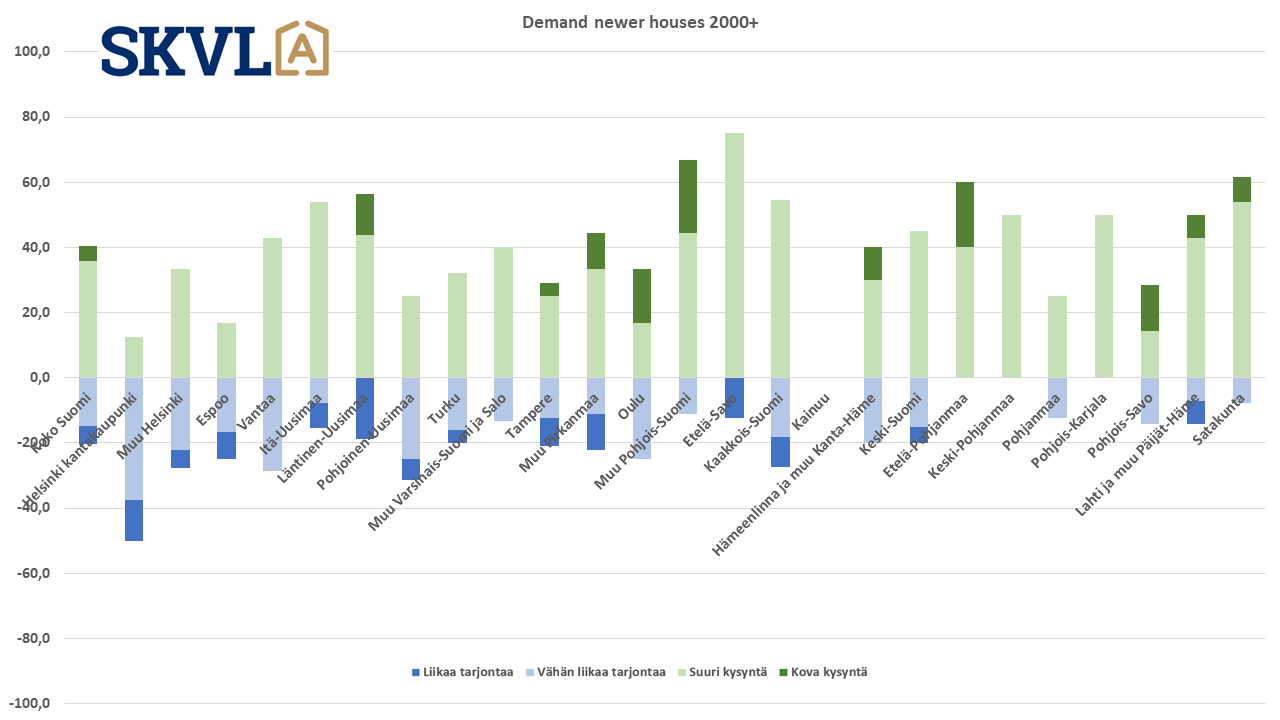

Turku

Larger apartments and detached houses in good condition are of interest. Inquiries have also started to come in about studio apartments in the city centre. There is a shortage of good terraced houses. Demand for rental housing has clearly improved, even though there is a lot of supply. There is very good demand for larger rental apartments.

Rest of Southwest Finland and Salo

Kaarina still has attractive, but longer-term consideration. The decision to sell and purchase takes longer. There are challenges in obtaining credit. In Raisio, trading has improved.

Tampere

In Tampere, the market situation is waiting. There are still some differences of opinion between sellers and buyers. The demand for small apartments is clearly lower. Homes that are in good condition and priced correctly sell out.

Rest of Pirkanmaa

The reasonably priced houses of the 2000s are selling, and the price level in renovation projects has fallen. People are prudent, go many times to see. There are challenges in financing. At Nokia, the market situation looks clearly better. In Pirkkala, housing sales have picked up.

Oulu

There is good demand for single-family houses, and the market for terraced houses is also recovering. Buyers are on the move, but studios and two-room apartments are the most challenging to sell. There is demand for large, fairly new family apartments. Similarly, apartments with their own yard sell well. Older apartments in blocks of flats in good condition in completely renovated housing companies are also sold more easily.

Northern Finland

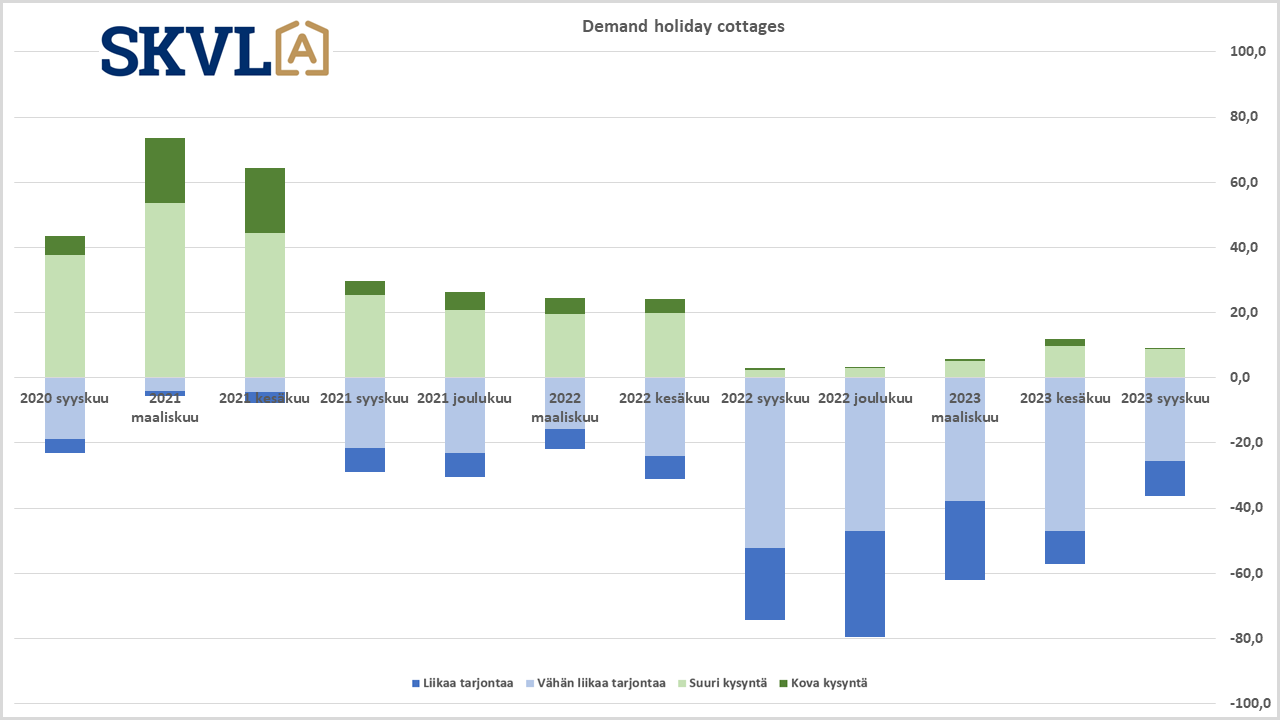

Demand is good in the Northeast region. Demand for sales and rental properties has recovered. In the autumn, an increase in demand for holiday homes is expected, especially in resorts.

Demand in Rovaniemi has grown almost normal with the autumn, but the forecast for winter is even calmer. Demand for detached houses and terraced houses of the 2000s.

South Savonia

Sales of free-time residences are proceeding normally. Interest rates have not so much affected the sale of free-time residences, because most often they are bought debt-free. There is clear caution in housing sales, but when pricing is right, the sale is good. In Pieksämäki, housing sales are quiet.

Southeast Finland

In the Lappeenranta region, the market situation is improving. Customers are more active and make decisions. There is still a lot of oversupply of small dwellings in blocks of flats.

Kainuu

Kajaani has a wide range of good offerings, but trade is still calm.

Hämeenlinna and the rest of Kanta-Häme

In Forssa, demand is quiet. There is calm demand in Hämeenlinna. Lammi, Hauho, Hämeenkoski and Padasjoki have better demand.

Central Finland

In Jyväskylä, trade has started to be slightly busier, willingness to buy has increased and caution has decreased. Terraced houses in particular are interesting, and the demand for electrically heated apartments has also improved clearly. Detached houses and terraced houses built in the 2000s are in the best demand and there is a good supply of them. Demand has also improved outside Jyväskylä, such as in Haukkala, Palokka, Muurame and Laukaa.

South Ostrobothnia

Good demand for affordable old housing, the most expensive a little less demand. Demand for investment housing low. Foreign buyers are now appearing and inquiries are focused on more affordable properties.

Central Ostrobothnia

The market situation is calm.

Ostrobothnia

August was good, towards late autumn the market calms down somewhat. Holiday homes will also continue to be available for sale. In Vaasa and Korsholm, it was busy in the summer and somewhat quiet in the autumn. Waiting for interest rates to fall. In Vaasa, young first-time buyers do not always find what they are looking for at a suitable price level.

North Karelia

In Joensuu, sales have been moderate, and there is also demand for larger and more expensive properties. The demand for new properties is very low. The demand for single-family houses is very good. Prices have fallen somewhat in Joensuu, Kontiolahti and Lehmo.

Northern Savonia

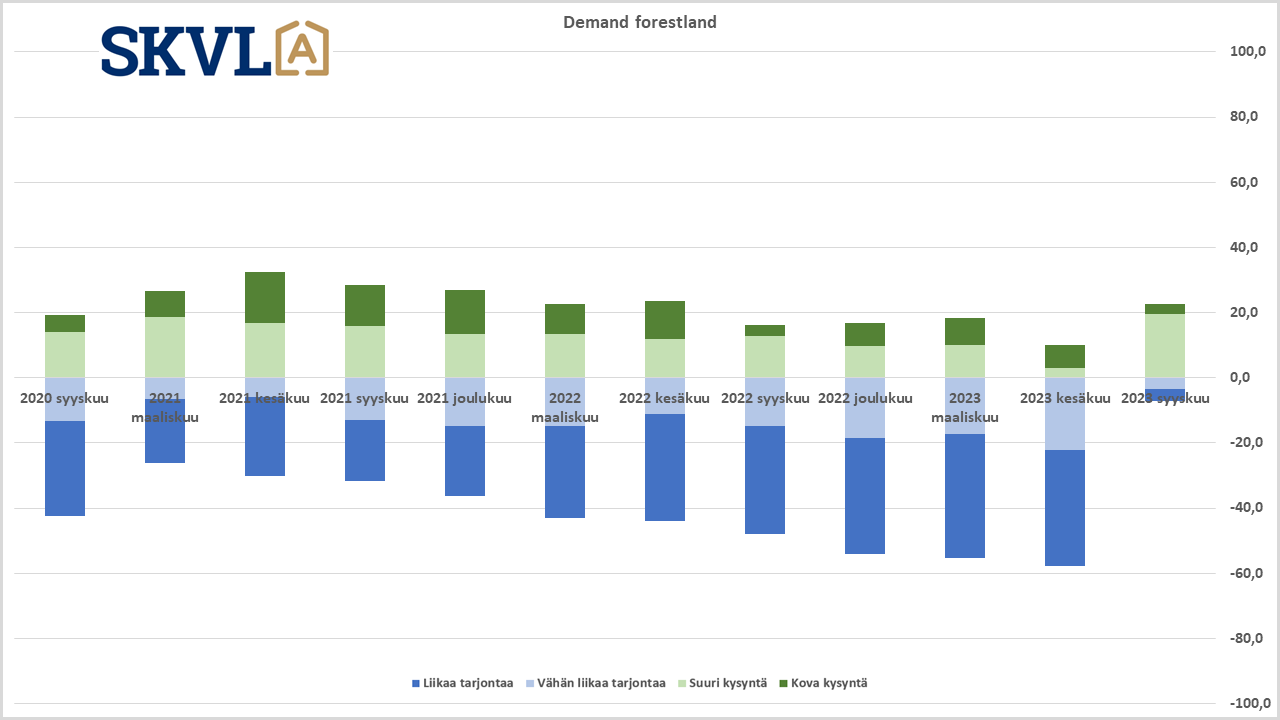

There is great demand for energy-efficient terraced houses and detached houses in good locations. Newer and smaller apartments in apartment buildings are also selling and investors have started to move. There are also many first-time homebuyers on the move, but there are problems with financing. The demand for more affordable housing is moderate. The demand for forests is very good. In Siilinjärvi, the focus of demand is on sites from the 2000s, and location is important. There is a lot of supply of houses from the 60s, 70s and 80s, but demand is lower. There is better demand for good renovated housing companies.

Lahti and the rest of Päijät-Häme

The market situation will improve somewhat. Trade volumes have increased. August and September were clearly better months, but there was some shortage of good sales targets. Strong fluctuations in demand from month to month. The situation is waiting.

Satakunta

For example, trade in the Kokemäenjoki valley has clearly increased. There is good demand for more affordable apartments in good condition. In the Pori area, the triangle is in high demand. Trade in Rauma is calm and expectant.